Why real estate prices are rising in Prague — this is a question we at Get Home hear from buyers, investors, and families trying to understand whether it is worth waiting for a decline. If you look at the market without emotion, the answer turns out to be fairly down to earth. In Prague, the following have been colliding for many years:

- strong internal demand,

- a growing population,

- the fragmentation of households,

- a chronically slow supply response.

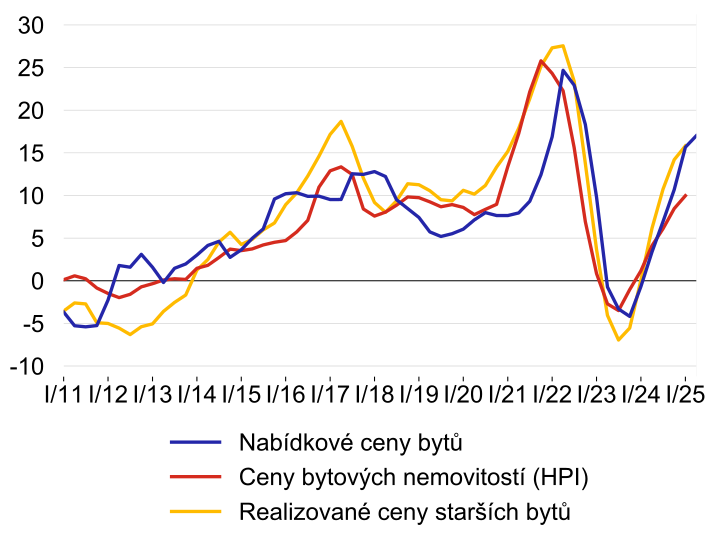

After the correction of 2022–2023, the market returned to growth again: according to ČSÚ, in 2024 the average price of an apartment in Prague reached CZK 115,889 per square metre, and according to ČNB, already in the first quarter of 2025 the apartment price index in the Czech Republic rose by 10% year on year.

Source: ČNB (Residential real estate prices are rising significantly, annual changes in %)

It is also important that this growth cannot honestly be explained by a single factor. It is impossible to reduce the whole story only to mortgages, only to foreigners, or only to a shortage of new projects. The Prague market is expensive precisely because several persistent reasons are operating at the same time and reinforcing each other.

That is exactly why even the pandemic, the energy shock, and the war did not reverse the trend for long, but only slowed it temporarily. The Czech National Bank (ČNB) spoke about this in general as well, noting the market’s return to a growth phase, while Deloitte directly points to the combination of high demand and limited supply.

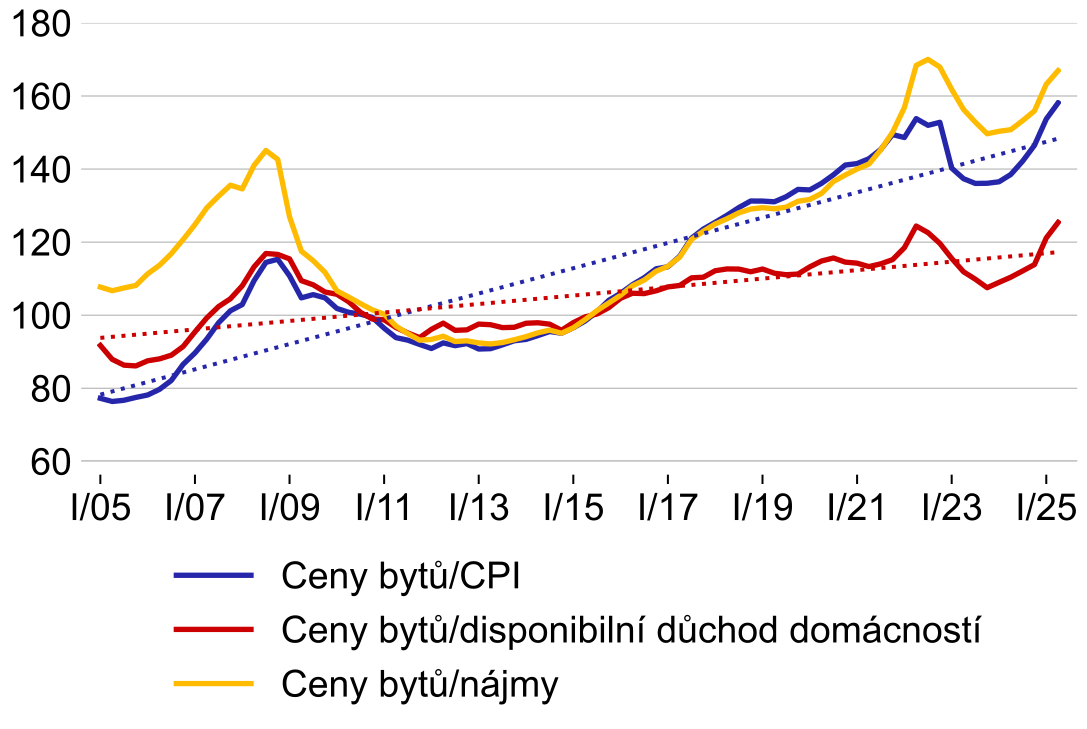

Source: ČNB (Real apartment prices exceeded the highs of 2022, housing affordability has recently been deteriorating indices (2015 = 100), long-term trends are indicated by the dotted line)

For us at Get Home, the key conclusion is simple. As long as Prague remains the country’s main economic centre, as long as people continue moving here, and the new construction market fails to keep pace with this need, prices will remain high.

The question today is no longer whether prices are rising by chance, but whether there are enough forces in the system capable of truly reversing that growth. Based on current data, we see that for now such forces are insufficient (ČSÚ).

Real estate prices in Prague and housing affordability rankings

Prague and the Czech Republic regularly appear in rankings with very poor housing affordability. The best-known example is the Deloitte Property Index (Deloitte): according to its data, residents of the Czech Republic need the equivalent of 13.3 annual gross salaries to buy a standard new 70 m² apartment, and this is the worst result among the countries included in the study. This fact in itself is important: it confirms that housing really remains expensive relative to incomes. But these rankings need to be read carefully, not literally.

The problem is that many international and media rankings compare nationwide salaries with real estate prices in Prague, while the Prague market lives by its own logic.

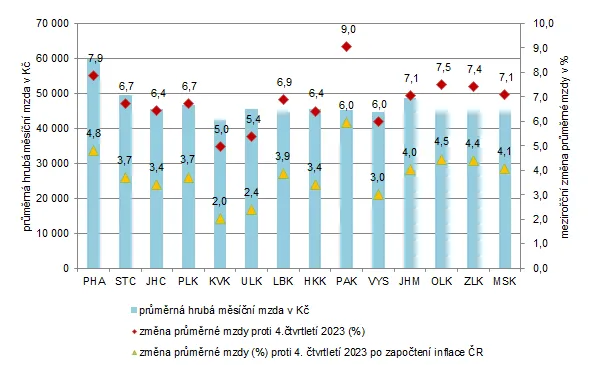

According to ČSÚ (ČSÚ), the average gross salary in Prague in 2024 was CZK 57,232, which was 24% above the national average, and in the detailed wage structure for Prague the average monthly salary of employees reached CZK 62,022.

Source: CSU (Average monthly gross salary in the 4th quarter of 2024)

In other words, using only the “average salary in the Czech Republic” to assess Prague affordability is methodologically convenient, but not always accurate.

In addition, some of these rankings are published by developer structures or studies focused primarily on the new-build market: in them, average incomes are compared with the cost of the average new apartment in Prague, although new apartments are generally more expensive than properties on the secondary market. That is why such calculations show market pressure well, but do not always fully reflect the situation across the entire housing stock of the capital.

There is also one more limitation. Official wage statistics describe salaried employees well, but they are worse at showing the real incomes of those who work as entrepreneurs, on a živnostenský list, or in mixed forms of employment. For Prague, this is especially sensitive because the capital concentrates business activity, while statistics simultaneously record a high wage level, a large number of economic entities, and a significant self-employed segment. Therefore, any housing affordability ranking is useful as an indicator of general pressure on the market, but not as an exact formula that can honestly describe the purchasing power of all groups in Prague.

Demand for housing in Prague is growing faster than it seems

The main factor behind rising prices is not abstract hype, but stable internal demand. In 2024, Prague’s population grew by another 13,148 people and reached 1,397,880 residents. The growth was driven primarily by migration. Even in the first half of 2025, when the pace was already weaker, Prague together with the Central Bohemian Region remained among the few regions where demographic pressure on the market did not disappear (ČSÚ). For housing, this is fundamental: if the city continues to attract people, base demand does not go anywhere.

At the same time, the market is under pressure not only from the number of residents, but also from the way people actually live. According to the census data from 2021, Prague had the lowest average number of people per apartment among all regions of the country, and 43.9% of occupied apartments were occupied by just one person. This is a very important detail. When the number of single-person and small households grows, the city needs more separate apartments even with moderate population growth. In such a case, demand increases faster than can be seen from demographics alone.

The same process can also be seen at the national level. ČSÚ notes that in the Czech Republic an average of 2.26 people live in one apartment, whereas in 1991 the figure was 2.76. At the same time, the average housing area per person increased to 38 m². In other words, society needs not just more apartments as units, but also more square metres per resident. For Prague, where the concentration of small households and mobile professionals is especially high, this automatically supports prices.

Foreigners in Prague’s real estate market: an important factor, but not the main reason

One of the most persistent myths sounds like this: prices in Prague are rising because housing is being bought up en masse by foreigners. In practice, such wording is too crude. Yes, foreigners play a noticeable role in Prague, and their presence in the city is indeed large. According to ČSÚ data, at the end of 2024 foreigners made up 25.3% of Prague’s population, and in absolute terms their number, excluding persons with asylum, reached 354,323 people. This is a lot, and this fact cannot be ignored.

But this statistic does not mean that foreign buyers are the ones dominating price growth.

First, the high share of foreigners among residents itself means that they are part of ordinary urban demand for living, renting, and buying, not an outside force that came to “break” the market.

Second, Czech sources and market reviews of recent years consistently note that investment demand for apartments is to a large extent also formed by Czechs themselves, and in 2025 ČNB specifically reacted דווקא to the growing share of demand for investment residential properties within the mortgage market.

Source: ČNB (The number of apartments owned by persons with permanent residence outside the territory of the Czech Republic has increased, however their share in the overall market remains low)

And this is confirmed by our daily practice at Get Home: in more than half of cases, Czechs come to apartment viewings, and they also more often become the buyers. The share of foreigners among retail buyers, in our experience, is roughly equal to or even lower than the share of foreigners living in Prague.

That is why we would formulate it more carefully. Foreigners are part of Prague demand, but not a universal explanation. When the population of a city is growing, jobs are concentrated there, business activity remains high, and at the same time housing supply lags behind, prices rise not because of one nationality of buyers, but because of the overall market imbalance. Personalising this problem is too politically convenient, but analytically it is a weak explanation.

The shortage of supply in Prague has been fuelling price growth for years

Demand would be a much less painful factor if supply responded quickly. But this is exactly where Prague runs into its systemic problem. Even after the reform of construction legislation and the launch of digital tools, the market did not see a sharp acceleration. The Ministry of Regional Development itself acknowledges that the digitalisation of the construction process was accompanied by serious difficulties: according to the ministry’s published survey, half of the surveyed authorities stated that after the launch of the digital system, construction procedures had rather slowed down, and only 6% saw acceleration.

Source: MMR (How do you assess the functionality of the Builder’s Portal compared to the situation shortly after the introduction of DSŘ (June 2024)?

If you look at real large-scale projects, the problem is even more visible. Smíchov City took about 15–16 years of preparation and approvals before reaching implementation. For Rohan City, preparation took around 13 years. These are not rare curiosities, but a symptom of how slowly the path from idea to construction moves on large sites in Prague (e15).

Source: E15 (A new Prague district, Smíchov City)

While a project spends a decade or more going through planning changes, approvals, objections, and appeals, the market continues to live with the current shortage.

There is also a second side to the problem: the cost of bringing new supply to market itself. Long timelines mean more expensive land, more expensive capital, and more regulatory risk.

On top of this come the prices of labour and materials. It is no coincidence that even major players publicly spoke in 2025 about postponing the launch of part of their projects because of overly expensive construction supplies and contract work.

For the market, this means not just an expensive entry point for new housing, but also a further squeeze on supply: if the launch of construction and sales is delayed, new apartments come to market later, which means the shortage persists longer and additionally pushes prices upward.

Mortgages in the Czech Republic remain accessible, and borrower quality appears resilient

Many expected that after the period of high rates, demand for purchases would weaken sharply. But the Czech market showed a more complex picture. ČNB kept the upper LTV limit for owner-occupied housing at 80% at the end of 2025, and 90% for borrowers under 36. The DTI and DSTI indicators for standard mortgages remained deactivated. This means the regulator does not consider it necessary to radically tighten access to mortgages for the main mass of home buyers.

Even the stricter restrictions of 2026 are aimed not at the whole market, but only at a relatively small part of investment mortgages. ČNB directly stated that the new rule with LTV 70% and DTI 7 concerns a comparatively small part of the mortgage market. In other words, the basic financing channel for owner-occupied housing in the Czech Republic remains open, which means there is no such cooling of demand that could sharply bring prices down.

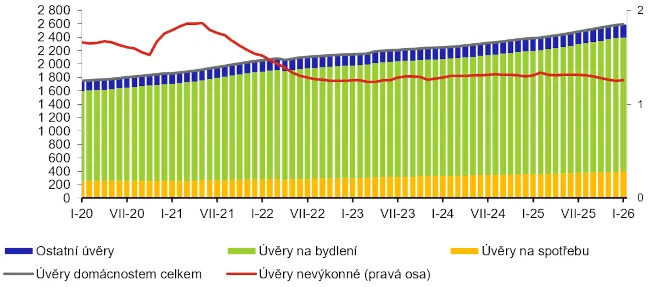

The quality of already issued loans is no less important. According to the banking statistics of ČNB, the volume of housing loans to households in January 2026 reached almost two trillion crowns, while the share of problem loans in this segment remains low by international standards.

Source: ČNB (Loans provided to resident households by purpose (CZK billions) and the share of non-performing loans (%)

In its financial stability reports, ČNB emphasises that banks maintain prudent lending standards, and systemic risks in the mortgage segment do not look like a trigger for a mass wave of defaults. This means the market is not receiving a large inflow of forced sales, which would usually be capable of putting significant downward pressure on prices.

Why Prague’s real estate market supports itself

The Prague market is strong not only because of the shortage of new construction, but also because of the cultural model of demand. According to the survey of the financial situation of households, around 73% of households in the Czech Republic live in their own apartment or house.

In addition, real assets, above all real estate, dominate the asset structure of Czech households: ČSÚ previously estimated their share at approximately 88% of total household wealth. This is a very important background for understanding the market. In the Czech Republic, real estate is not a niche asset, but a central element of family capital.

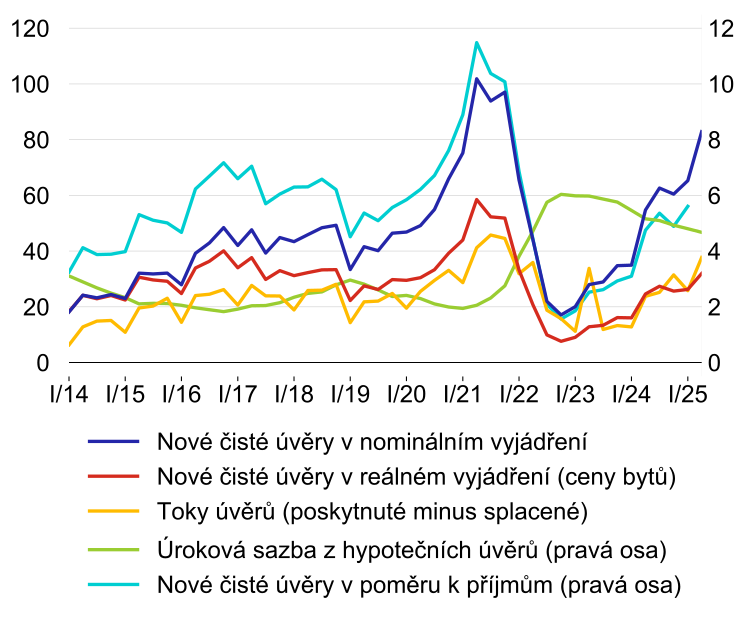

This logic also gives rise to steady investment demand for small apartments in Prague. ČNB records growing demand for loans financing investment residential real estate, as well as growth in household investment in housing.

Source: ČNB (Demand for mortgage loans is growing rapidly, and their volumes this year are the second highest in history; relative to incomes they are at pre-Covid levels)

In practice, this means that for many local families, an apartment in the capital remains not just a place to live, but also a way to preserve capital, prepare housing for children in the future, or secure income and flexibility in retirement. As long as such a model remains widespread, the market receives additional support from within, not just from classic investors.

This also gives rise to a political paradox. Society wants more affordable housing, but most households are already tied in one way or another to the value of their own real estate. Therefore, radical measures that could really and quickly put strong downward pressure on prices almost always turn out to be politically extremely uncomfortable.

Against this background, partial reforms, failures in digitalisation, and slow changes in supply do not break the market, but only support its current inertia. That is exactly why we have been observing the same trend for so long: Prague is becoming more expensive not despite the system, but in many ways because of how this system is structured.

Conclusion

If everything is reduced to one idea, then prices in Prague are rising primarily because internal demand in the capital remains strong, while supply is trying to catch up too slowly and at too high a cost. Housing affordability rankings show a real problem, but they do not always describe Prague itself accurately.

Foreigners are present in the market, but they do not explain it entirely. Demography, migration, the fragmentation of households, the culture of property ownership, a resilient mortgage market, and bureaucratic constraints together create a structure in which falling prices become more the exception than the base scenario.

At Get Home, we believe that the Prague market must be discussed precisely through this combination of factors. Then it becomes clear why even strong external shocks have so far been unable to reverse the trend for long. And that is exactly why, in our recent article about the role of ČNB in 2026, we also noted that individual regulatory measures may cool part of the demand, but by themselves they do not solve the problem of supply shortages and the long approval process for new projects. As long as these basic causes remain, the Prague market will continue to stay expensive.