Real Estate in the Czech Republic: Will the New Law Stop Price Growth?

Real estate in the Czech Republic has once again become the number one topic for buyers, investors, and those who have long been waiting for the right moment to make a deal. As of April 1, 2026, the rules on the market are indeed changing, but let us clarify one important point right away: in everyday language this is often called a new law, although legally it is more accurate to speak of a new recommendation regime of the Czech National Bank, that is, ČNB. This does not concern all mortgage buyers, but rather the financing of investment properties, including the third and each subsequent residential property.

Source: ČNB (Financing of investment properties)

The main question is simple: can this step really stop price growth? In our view at Get Home, the answer is скорее no. The reason is that the new tightening affects only part of demand, while prices in the Czech Republic are rising not because of a single factor, but because of a combination of a long-standing supply shortage, demographic pressure, a slow permitting process, and rising construction costs.After the correction of 2022–2023, the market did in fact return to growth fairly quickly, and the first signs of a recovery in price dynamics were recorded as early as the end of 2023. According to the Deloitte Real Index (Deloitte), in the fourth quarter of 2023 the average price of sold apartments in the Czech Republic increased by 6.9 percent quarter on quarter, and in Prague by 6.5 percent. In 2024, the growth was already confirmed in official statistics as well: according to ČSÚ (ČSÚ), the average apartment price across the Czech Republic rose by 6.0 percent year on year and reached CZK 63,521 per square meter, while in Prague the average price level stood at CZK 115,889 per square meter. Moreover, in 2025 the trend intensified: ČNB (ČNB) indicates that in the first quarter of 2025 the apartment price index rose by 10 percent year on year. Therefore, it is more accurate now to say not that the new restrictions will stop the market, but that they may only slightly slow price growth in the investment purchase segment.

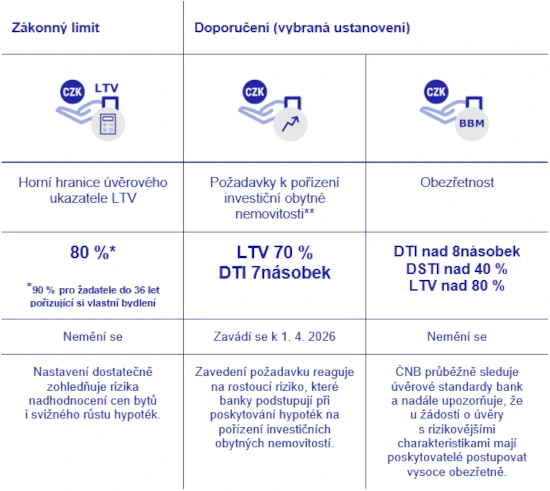

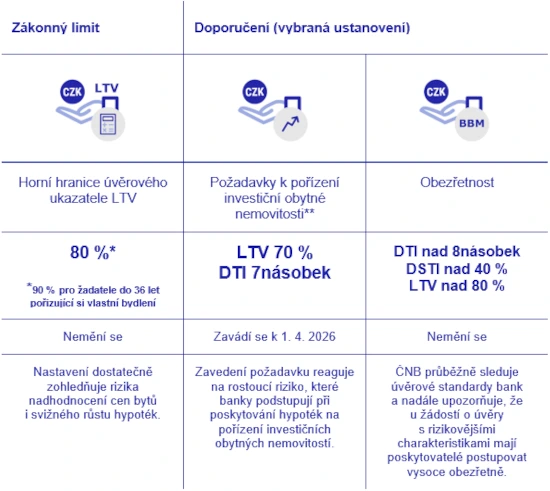

ČNB’s New Regime from April 1, 2026: What Changes for Investment Apartments

Put simply, ČNB divides purchases into two large groups:

- the first group is housing for owner-occupation,

- the second is investment residential real estate.

A property is considered an investment property if the borrower explicitly states that it is being purchased not for owner-occupation, if expected rental income is taken into account when calculating income, and also if the borrower already owns two residential properties and is acquiring a third or subsequent one. It is precisely this segment that falls under the new tightening. There are two key figures:

- the first is LTV 70 percent, meaning that the mortgage must cover no more than 70 percent of the collateral value. Put simply, the buyer must contribute at least 30 percent in own funds,

- the second is DTI 7, meaning that the borrower’s total debt must not exceed seven times their net annual income.

For ordinary owner-occupied housing, the basic limits remain unchanged: LTV 80 percent, and for buyers under 36 years old, if the property is intended for owner-occupation, up to 90 percent. DTI and DSTI for standard mortgages remain deactivated. In practice, the impact of the LTV restriction is not as straightforward as it may seem from the formula of “30 percent own funds.” The Czech National Bank (ČNB) defines LTV as the ratio of the loan amount to the value of the mortgaged property, and the ČNB methodology expressly states that the value of the collateral may include all residential properties securing the given loan, not only the apartment being purchased. This means that for some investors who already own other properties and whose value has increased in recent years, the new 70 percent LTV limit may prove less strict than it appears at first glance: in certain cases, the bank may assess the transaction with additional collateral taken into account, rather than relying solely on the volume of the client’s available cash funds. At the same time, it would be too categorical to conclude that this measure will have no impact on the market at all. First, along with LTV, a DTI 7 restriction is also being introduced for investment properties, and this cannot be offset by additional collateral. Second, the possibility of using another property as collateral depends on the specific bank, the structure of existing obligations, and the collateral assessment. In addition, if the same property already secures a previously granted loan, not its full value is taken into account, but only the portion of the collateral that can be allocated to the new loan. Therefore, it is more accurate to say that the new ČNB regime (ČNB) does not automatically block investment purchases, but makes them more selective and more complex from the standpoint of bank approval. Therefore, for those planning to acquire an investment property under the previous financing conditions, it is important to aim for signing the loan agreement before April 1, 2026. This concerns not only the stricter LTV 70 limit, but also the introduction of the DTI 7 ratio for investment purchases, meaning a restriction under which the borrower’s total debt must not exceed seven times their net annual income (ČNB, ČNB).

Source: ČNB (LTV, DTI indicators)

This is precisely the parameter that may prove a more significant restriction for some investors, because additional collateral may affect LTV, but it does not change the ratio between total debt and income. Therefore, when purchasing a third and each subsequent residential property, the issue will no longer be only the size of the down payment, but also whether the borrower fits within the new debt burden limit established by ČNB (ČNB).

Why Real Estate Prices in the Czech Republic Rose for Almost Twelve Years

The Czech real estate market remains highly inertial, so the impact of the new restrictions is unlikely to reverse the price trend. After the correction of 2022–2023, prices returned to growth again: according to ČNB, already in the first quarter of 2025 the residential real estate price index rose by 10 percent year on year, and real apartment prices in 2024 and early 2025 exceeded the highs of 2022 (ČNB).

Chart 1 — Residential real estate prices are rising significantly, year-on-year change in %, source: ČSÚ

Chart 2 — Real apartment prices have exceeded the highs of 2022, while housing affordability has deteriorated recently. Indices (2015 = 100), long-term trends are shown with dotted lines, source: ČSÚ

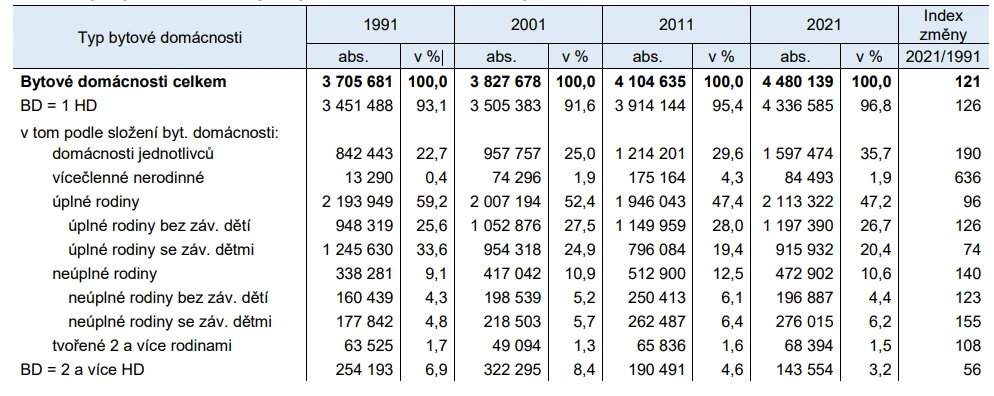

This means that the market is now not in a phase of prolonged correction, but in a phase of recovery and renewed growth, supported by limited supply and resilient demand (ČNB). If you look not at a single quarter but at the longer cycle, this is precisely the multi-year upward trend that market participants are now talking about. The first reason for this trend is demand that year after year does not meet sufficient supply. According to ČSÚ, by the end of 2024 the population of the Czech Republic was 371.2 thousand people larger than at the beginning of 2015. This does not mean that every new resident immediately buys an apartment, but it does mean that pressure on the rental, purchase, and housing-change market is growing. At the level of Prague, this effect is especially visible: in an interview with Aktuálně.cz, it was estimated that over the last 20 years the city’s population had increased by around 300 thousand people, while the annual volume of new construction remains limited. At the same time, pressure on the market is intensifying not only because of the growing number of residents, but also because of changes in the structure of households themselves. According to the Czech Statistical Office, in 2021 the average size of a housekeeping household in the country fell to 2.15 people, nearly 40 percent of households consisted of single-person households, and the most common households were those with one or two people (ČSÚ). This means that even with moderate population growth, the need for housing increases faster, because the same number of residents requires a larger number of separate apartments. The same conclusion is confirmed by data on the actual use of the housing stock. According to ČSÚ, the average number of residents per apartment decreased from 2.76 people in 1991 to 2.26 people in 2021, while the average total housing area per person increased from 25.5 to 38.0 square meters.

Table 1. Dynamics of household structure in apartments by type between the 1991 and 2021 censuses. Source: ČSÚ

In other words, demand is now shaped not only by the number of apartments as housing units, but also by the need for a larger number of square meters per person. For large cities, above all Prague, this is especially important, because this is where single-person households, single-parent families, and other living arrangements that increase the load on the market are more often concentrated, even without a sharp jump in the total population. The second reason is the very slow response of supply. The Czech Ministry of Regional Development (MMR) itself acknowledges that the length of permitting processes remains one of the main problems, which is precisely why reforms of construction law are being promoted. Formally, the new construction law did indeed establish specific time limits for issuing permits: 30 days for simple constructions and 60 days for the others, with the possibility of extension by up to another 60 days. However, the mere fixing of deadlines does not mean an automatic acceleration of the process. The law expressly allows for extensions, and if proceedings are suspended due to deficiencies in the application, the time limit starts anew once those deficiencies are remedied. The appeal stage also remains in place, with its own procedural deadlines. Therefore, the key problem of the Czech market lies not only in the presence or absence of formal deadlines, but in the fact that complex projects still go through lengthy approvals, administrative disputes, and multi-stage procedures (MMR). This is clearly visible in Prague’s largest brownfield projects. Smíchov City reached the construction stage after roughly 15–16 years of preparation and permitting processes, while Rohan City started after 13 years of preparation.

The second office building from the initial phase of the Rohan City project, designed by architect Jakub Cigler. Source: IPR archive

A similar pattern can be seen in the area of Nákladového nádraží Žižkov: Sekyra Group’s key deal with České dráhy regarding the southern part of the site was closed only in April 2025, simultaneously with the approval of an important change in planning documentation.

Žižkov Freight Station (Nákladové nádraží Žižkov). Source: Profimedia.cz

Therefore, it is more accurate to say not that the new law has already solved the problem of supply shortage, but that even after the reform and the launch of digital tools, the market still faces lengthy permitting procedures, and the expected sharp acceleration has not yet occurred (e15, e15, e15). The third reason is related to the economics of construction. Rising developer costs are confirmed not only by ČSÚ statistics, but also by the behavior of the market’s largest participants. At the end of 2025, Central Group announced that it was postponing the launch of new projects by about a year, explaining this by unacceptably high prices for construction work and materials from contractors. In January 2026, the company additionally stated that it would be ready to resume part of the projects only if the cost of construction supplies fell by at least 10 percent.

Central Group announced that it was postponing the launch of new projects by about a year

This shows that the problem of high construction costs is already affecting not only cost price, but also the timing of bringing new projects to market, and thus further restricts the supply of new housing. In addition, the problem of prepared plots and utility networks remains. It is enough to look at MMR programs supporting technical infrastructure: the state separately finances the creation of roads, water supply, and sewerage for future residential development in order to expand the supply of prepared plots. Part of this problem is being addressed through the redevelopment of urban brownfield areas, which in the Czech Republic are increasingly seen as one of the main reserves for residential and mixed-use development, especially where basic infrastructure already exists. That is why in MMR’s strategic documents revitalizace brownfields is linked not only to the renewal of the urban environment, but also to limiting the excessive expansion of cities into new territories. At the same time, the shift to brownfield development does not by itself eliminate the problem instantly: such sites also require preparation, documentation, financing, and regeneration, so the shortage of areas ready for rapid development remains on the market.

Will the New Tightening Stop Real Estate Price Growth in the Czech Republic

Most likely not. And this is not an attempt to calm the market, but rather a fairly sober assessment of the scale of the measure. ČNB itself says that the recommendation concerns a relatively small part of the mortgage market. The new requirements do not change the rules for buyers of homes for owner-occupation, which means they do not affect the main layer of demand. In essence, the regulator is selectively raising the barrier for the most heavily indebted investors, rather than cooling the entire real estate market in the Czech Republic.  In addition, some investors will be able to adapt quite legally and without formal workarounds. Some will contribute more of their own funds. Others will be able to fit within the new DTI 7 limit thanks to higher documented income, including income from housing already being rented out. At the same time, ČNB itself also classifies as investment purchases those cases in which the bank takes into account the expected rental income from the acquired property when assessing creditworthiness. This means that for some borrowers, the key issue will no longer be only the size of the down payment, but also how the bank assesses their total documented income and overall debt burden. Therefore, it is more accurate to say that the new rule does not close the market completely, but makes the approval of an investment mortgage more dependent on the borrower’s income structure and the quality of the supporting documentation. The new restrictions will affect different investors in different ways. As regards LTV 70, their effect may be weaker for those who already own other residential real estate and can offer the bank additional collateral: the ČNB methodology allows the value of all residential properties securing the given loan to be taken into account, although if a property is already being used as collateral for another loan, only the corresponding part of its value is included in the calculation. Therefore, in a number of cases an investor will be able to reduce the effect of the new LTV limit not through own funds, but through additional collateral. However, this does not отменяет the DTI 7 restriction, which depends not on the collateral, but on the ratio of the borrower’s total debt to annual income. That is why for some investors the key restriction will be not LTV, but DTI.For non-purpose loans secured by housing, the regulator even recommends cautiously assuming by default that the loan is investment-related if the bank sees no evidence to the contrary. In other words, room for maneuver remains, but it is no longer as broad as before. Our conclusion at Get Home is this: with a high degree of probability, this step will not cause prices to fall across the Czech Republic. The market has too many strong underlying factors supporting prices, while the tightening of the rules affects only one, and not even the broadest, segment of demand. In the short term, however, the market may become calmer specifically in the area of investment purchases financed by mortgages. And that, in turn, may slow the pace of price growth for several months, especially where the share of investor transactions has traditionally been higher. This is a market-based assessment grounded in the scale of the measure and in the fact that the reasons for rising prices lie much deeper than a single mortgage filter.

In addition, some investors will be able to adapt quite legally and without formal workarounds. Some will contribute more of their own funds. Others will be able to fit within the new DTI 7 limit thanks to higher documented income, including income from housing already being rented out. At the same time, ČNB itself also classifies as investment purchases those cases in which the bank takes into account the expected rental income from the acquired property when assessing creditworthiness. This means that for some borrowers, the key issue will no longer be only the size of the down payment, but also how the bank assesses their total documented income and overall debt burden. Therefore, it is more accurate to say that the new rule does not close the market completely, but makes the approval of an investment mortgage more dependent on the borrower’s income structure and the quality of the supporting documentation. The new restrictions will affect different investors in different ways. As regards LTV 70, their effect may be weaker for those who already own other residential real estate and can offer the bank additional collateral: the ČNB methodology allows the value of all residential properties securing the given loan to be taken into account, although if a property is already being used as collateral for another loan, only the corresponding part of its value is included in the calculation. Therefore, in a number of cases an investor will be able to reduce the effect of the new LTV limit not through own funds, but through additional collateral. However, this does not отменяет the DTI 7 restriction, which depends not on the collateral, but on the ratio of the borrower’s total debt to annual income. That is why for some investors the key restriction will be not LTV, but DTI.For non-purpose loans secured by housing, the regulator even recommends cautiously assuming by default that the loan is investment-related if the bank sees no evidence to the contrary. In other words, room for maneuver remains, but it is no longer as broad as before. Our conclusion at Get Home is this: with a high degree of probability, this step will not cause prices to fall across the Czech Republic. The market has too many strong underlying factors supporting prices, while the tightening of the rules affects only one, and not even the broadest, segment of demand. In the short term, however, the market may become calmer specifically in the area of investment purchases financed by mortgages. And that, in turn, may slow the pace of price growth for several months, especially where the share of investor transactions has traditionally been higher. This is a market-based assessment grounded in the scale of the measure and in the fact that the reasons for rising prices lie much deeper than a single mortgage filter.

When Is the Best Time to Buy Real Estate in the Czech Republic in 2026

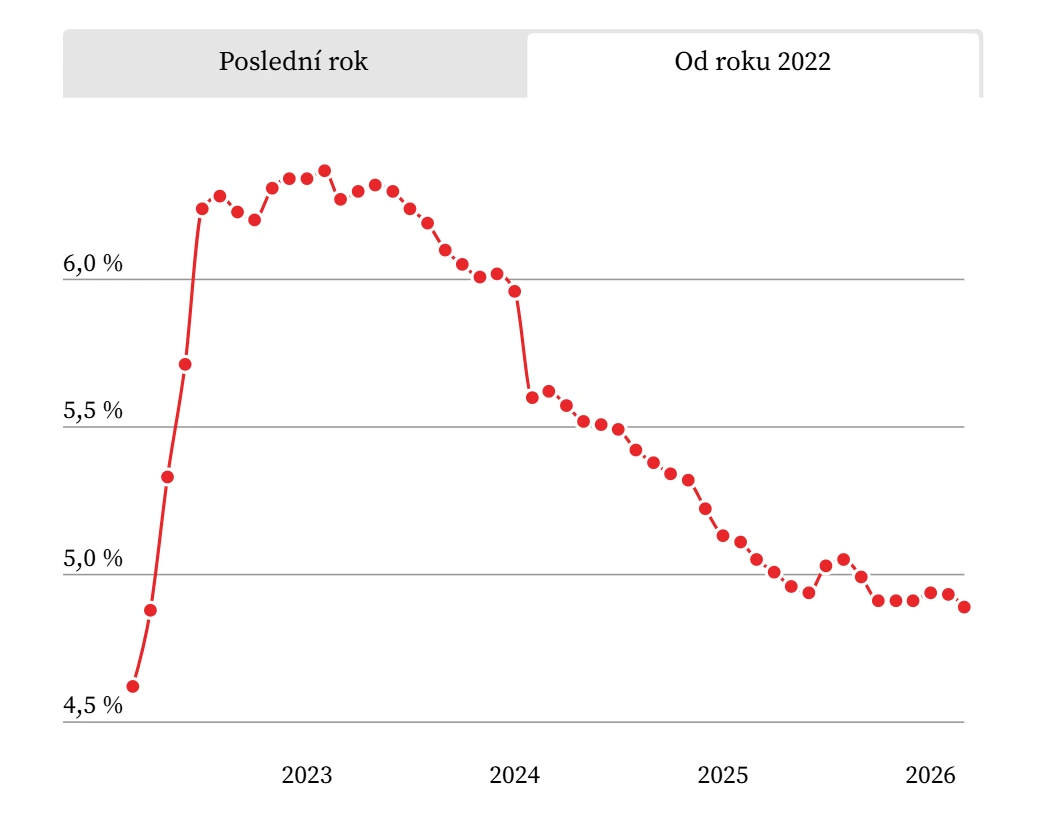

Looking at the coming months, a window of opportunity may indeed open from May or June through September. Here is why. First, the pre-April rush from those trying to make it under the old conditions will have subsided by then. Second, the new requirements will remove part of the overheated investment demand. Third, at the beginning of March 2026 mortgage rates did in fact fall below the psychological threshold of 5 percent: according to the Swiss Life Hypoindex, the average offered rate declined to 4.89 percent.

Author: Aleš Ligas | Source: Swiss Life Hypoindex | Note: since February 2022, the Hypoindex methodology has been changed.

However, further rate cuts came into question, since analysts were already linking subsequent dynamics to geopolitics in the Middle East, rising oil prices, and possible stronger inflationary pressure (e15). We would describe this period not as a time of cheap real estate, but as a time of calmer negotiations. That is an important distinction. The market is under no obligation to lower prices simply because one group of buyers has become harder to finance. But after April 1, competition for some properties may become less tense, while buyers with solid approval and a clear strategy will have more room to choose. That is why, in practice, the period from late spring to early autumn looks like a logical moment to enter the market. This is our team’s forecast assessment, not a promise of an overall price decline.Those who are buying an investment apartment with a mortgage and are counting on the old conditions definitely should not delay. The benchmark remains signing the loan agreement before April 1, 2026, but in practice it is better to act in advance, because ČNB has already made it clear to banks that it does not welcome delaying the transition. If, however, you are buying a home for your own residence, the rules remain softer, and here what matters is not rushing because of a date, but rather high-quality preparation of the transaction, a proper review of the property, and a strong negotiating position. You can find current options and go through this process without unnecessary noise together with Get Home. In short, the picture looks like this: the new ČNB tightening does not turn the market downward, but it may well cool specifically mortgage-backed investment purchases somewhat. Therefore, for some clients it is important to act before April 1. For some buyers, on the contrary, a more comfortable negotiation period may begin after April. And it is precisely these phases of the market that we at Get Home consider the most interesting: when the panic has already passed, while the fundamental demand for quality real estate in the Czech Republic has not gone anywhere.